Mitigating Non-Linear Risk: A Structural Analysis of the OrderX Multi-Band Delta Hedging Engine

Published by: OrderX

•

Conquering volatility in digital asset markets requires an institutional focus on execution optimization. For asset allocators managing cross-margined derivatives portfolios, manual delta management introduces non-market risks: execution latency, spread slippage, and cognitive processing fatigue. When market volatility expands, the time delayed between identifying a delta imbalance and executing the hedge invariably degrades the trade’s structural edge.

To eliminate this operational friction, OrderX has deployed an automated, production-grade Delta Hedging (DH) Engine. This analysis reviews the execution metrics from a 72-hour continuous production sandbox validation designed to test the platform’s multi-band routing logic under live market conditions.

Conquering volatility in digital asset markets requires an institutional focus on execution optimisation. For asset allocators managing cross-margined derivatives portfolios, manual delta management introduces non-market risks: execution latency, spread slippage, and cognitive processing fatigue. When market volatility expands, the time delayed between identifying a delta imbalance and executing the hedge invariably degrades the trade’s structural edge.

To eliminate this operational friction, OrderX has deployed an automated, production-grade Delta Hedging (DH) Engine. This analysis reviews the execution metrics from a 72-hour continuous production sandbox validation designed to test the platform’s multi-band routing logic under live market conditions.

The Sandbox Architecture and Parameter Constraints

The validation test was executed within a controlled production environment over a 3-day runtime duration. The core objective was to stress-test the algorithm's capability to defend an options portfolio's Greeks against rapid intra-day underlying price fluctuations without incurring toxic execution slip or API rate-limit degradation.

Testing Parameters:

Underlying Asset: ETH-PERPETUAL (Deribit)

Initial Position Setup: Long ETH Call Option Exposure

Hedge Trigger Threshold: Fixed 0.3% price variance intervals

Execution Profile: Delta Stream Continuous Mode

Platform Runtime: 2 Days, 22 Hours, 25 Minutes

Execution Dynamics and Micro-Volatility Extraction

Over the course of the 72-hour testing window, the underlying market experienced repeated direction changes. Rather than allowing the delta of the call option to drift into over-exposed or under-exposed regimes, the OrderX engine systematically adjusted the portfolio's net profile.

The system processed and filled 203 individual limit orders seamlessly.

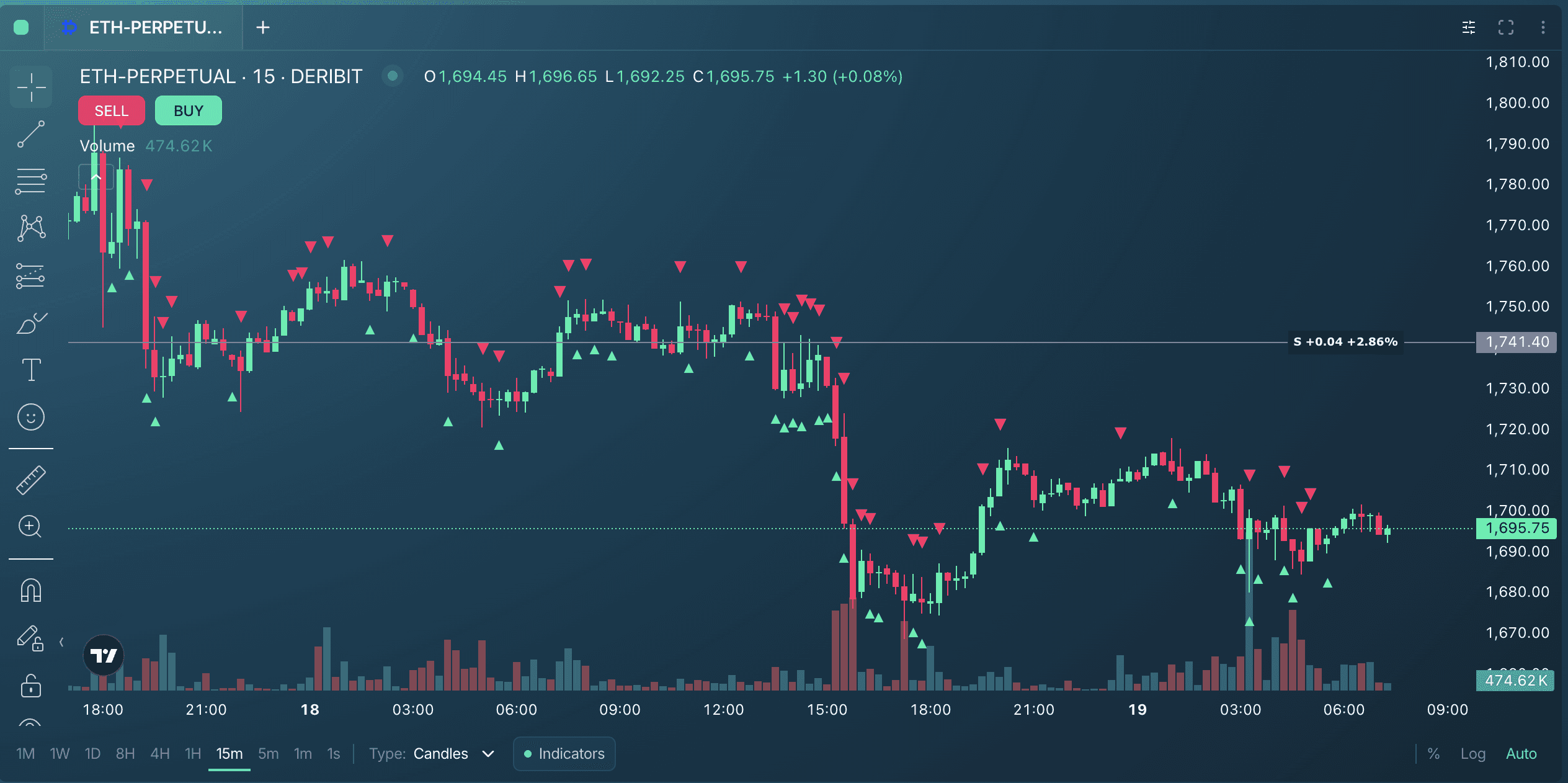

Systematic Rebalancing Visualisation

The engine's ability to accurately pinpoint structural pivots on the asset's micro-trend lines is mapped directly onto the execution history chart below:

Figure 1: Comprehensive trade execution matrix demonstrating automated buys (green triangles) and sells (red triangles) mapped against 15-minute intervals.

By executing hedges on precise 0.3% movements, the algorithm smoothed out the variance curve of the strategy. Instead of experiencing the typical drawdowns associated with delayed macro-hedging intervals, the constant rebalancing extracted localised market micro-trends directly into net equity, resulting in a ~15% capital optimisation inside the test portfolio environment.

Resolving the Core Institutional Pain Points

Standard algorithmic execution engines routinely fail institutional allocators in three key areas: fee structures, execution delay, and configuration complexity. The OrderX engine addresses these vulnerabilities directly through its core architecture.

1. Eliminating Taker Spread Bleed

Desks that run basic delta-hedging scripts often rely on market orders to clear out delta imbalances during high-velocity price moves. This results in severe fee penalties. The OrderX engine utilizes advanced Limit Chase and Post-Only Limit logic.

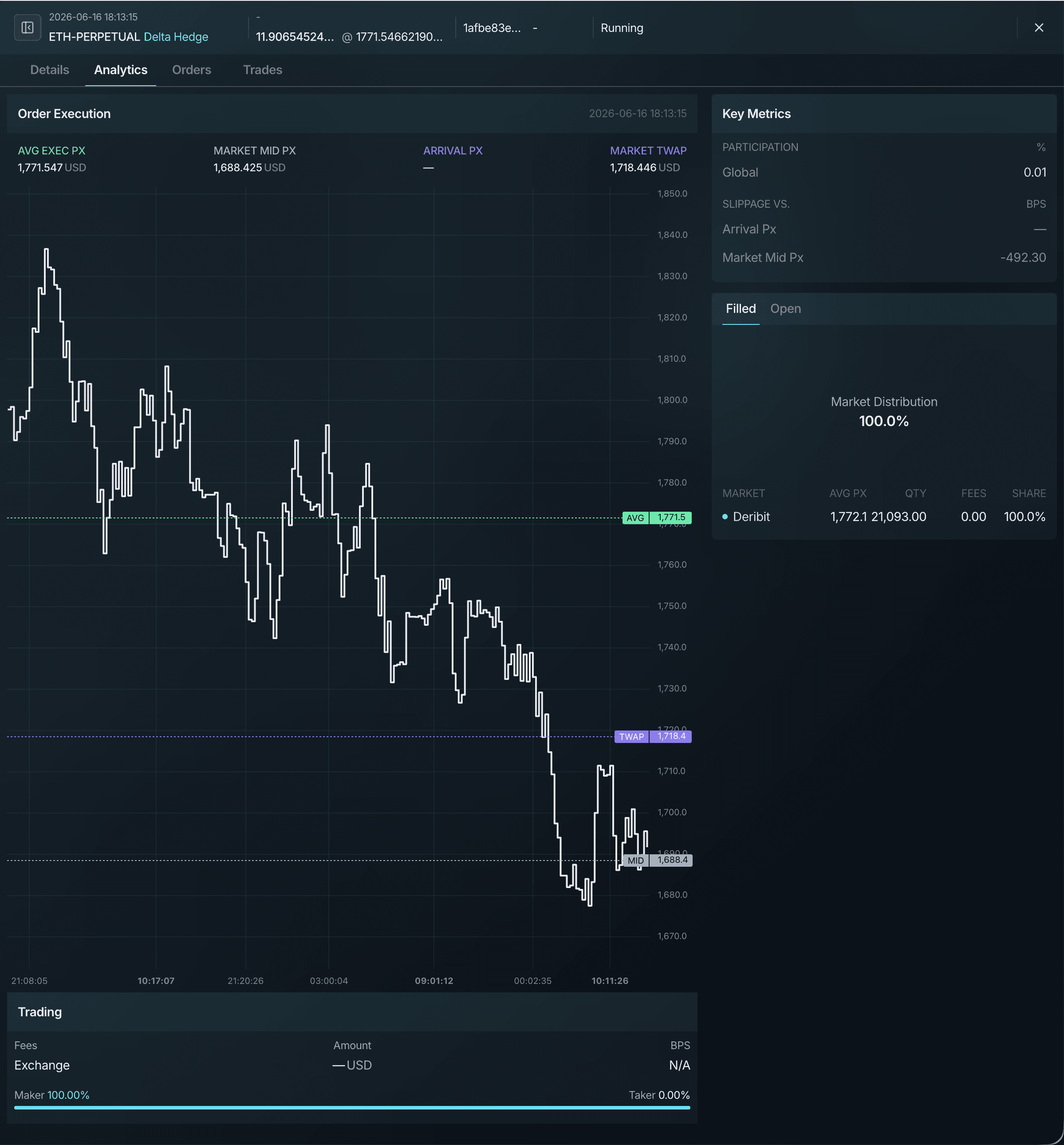

As documented in the platform's execution analytics, 100% of the 203 executed orders were filled as Maker volume. This means the platform actively earned market-making rebates or completely bypassed taker fees, ensuring that high-frequency rebalancing acts as an equity driver rather than a cost center.

Figure 2: Execution analytics panel showing a 100.0% Maker distribution across all routed volume, completely insulating the account from taker fee penalties.

2. Multi-Band Priority Routing

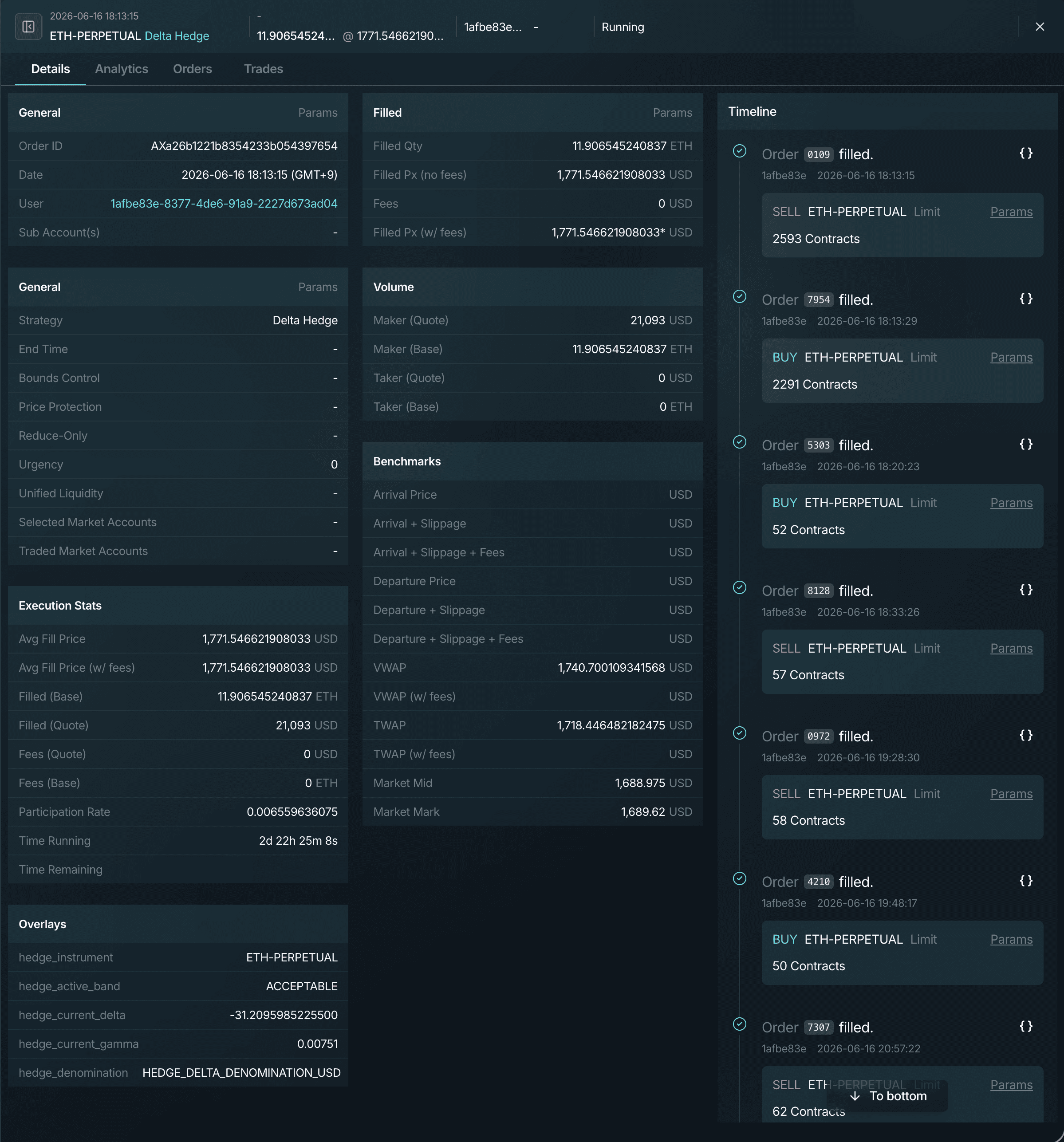

The behavioural psychology of an institutional trader involves a continuous trade-off between risk tolerance and urgency. The OrderX DH engine introduces a tiered priority matrix ("Acceptable Dead-Bands" and "Delta Bands") that mirrors this exact cognitive process.

The Acceptable Dead-Band: A customisable range where the algorithm remains passive, preventing unnecessary order adjustments and saving execution costs when the market chops sideways.

Tiered Priority Bands (Low to High): If the asset's delta breaches the dead-band, the engine scales its execution aggression. Traders can set closer bands to execute via passive limit orders, while wider, high-urgency bands utilize active TWAP or aggressive limit-chasing strategies to protect the desk against sudden, black-swan liquidation events.

Figure 3: Operational dashboard detailing active Greek tracking, underlying asset exposure, and real-time execution participation rates.

Step-by-Step Configuration Blueprint

To understand how seamlessly this engine integrates into existing workflows, our engineering team put together a comprehensive 5-minute technical walkthrough. This video covers configuring dead-bands, choosing between Delta Stream and Interval-based rebalancing modes, and deploying multi-tier execution speeds.

Conclusion: Process Over Luck

For sophisticated allocators managing capital scale, performance is a direct product of operational infrastructure. The 15% sandbox return achieved during our 3-day validation test serves as empirical proof that automating micro-hedging at tight intervals significantly lowers portfolio variance while protecting core equity.

The OrderX Delta Hedging engine will be available to use at launch and during our private beta test.

If you are interested in getting early access drop your email on our website: https://orderx.com/#get-started

A new way to

trade is here.

OrderX equips serious traders with the tools they’ve been waiting for Structured execution, integrated systems, and built-in intelligence.